How to not pay for a ticket to festivals big and small.

I love music festivals. But they aren’t cheap. One-day events can easily cost more than £80 after fees (those damn fees!), and you’ve got to factor in travel, food and drink on top. And obviously it’s much more for weekend festivals.

This means I’m always looking for deals and ways to save on festivals, but if money really is tight yet you have the time, then it’s well worth looking into volunteering.

Essentially in exchange for a shift or two (or three if it’s a longer festival), you get free entry to the festival. Yes, you are working, so you might miss some of the action, but it could easily be saving you hundreds of pounds.

What volunteers do at festivals

If you’ve ever been to a festival, you’ve seen the type of jobs volunteers do. There are those scanning tickets and tying wristbands. There are people pulling pints. There are others picking up rubbish and recycling. And there are some just generally helping out by giving information.

Shifts tend to be seven or eight hours long. Though these are assigned in advance, it looks like at most festivals it’s possible to switch with other volunteers if they agree – just in case your favourite band clashes with the time you are working.

For longer festivals you may be required to work one night shift, and you might be working far away from the stages. Day festivals shifts tend to end at 8pm so you’ll be able to catch the headliner.

You also usually need to attend some training, and some festivals require volunteers to attend a day or two before the masses arrive.

Festivals you can volunteer at

There are dozens of festivals running in 2025, and I’ve seen opportunities including:

Glastonbury (waiting list only for 2025 as of May)

Leeds/ Reading Festival

Isle of Wight Festival

BST

All Points East

Download

Boardmasters

Latitude

Camp Bestival

Boomtown

Latitude

If you really want to get one of the bigger events you’ll want to keep an eye on registrations which tend to open in the new year. You may also have to have volunteered at a smaller one first.

You often get secure camping, guaranteeing you a decent spot that isn’t miles away from the action – and possibly some exclusive showers and toilets. When you’re working you’ll probably get a free meal too, saving some extra cash.

Some festivals will allow you to bring children with you too – though it depends on each event.

Volunteering requirements

You will need to be over 18 at most if not all festivals in order to volunteer and have proof you can work in the UK.

You also need to pay a refundable deposit, which is usually the equivalent of the ticket price. There’s a good reason for this – it stops people using volunteering as an opportunity to get tickets to sold out events and not turning up for their shifts. But it does mean you need to send cash up front. You may also have to wait up to 30 days for the deposit to be refunded.

Some roles require experience, such as bar work, though that depends on the festival. The most popular festivals might also request you work another festival in the same year too.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

How to apply for festival volunteering

You can check out the information pages at different festivals, or take a look at one of the following sites. Some festivals offer different opportunities through different organisers. For example, you can volunteer for Reading or Leeds with either Hotbox or Oxfam.

If you’re applying with friends you can ask for shifts together (or at the same time) on the application.

Most are first come first serve, so the earlier you apply the better.

If you go via the likes of Oxfam or My Cause then you’re also helping charities, which sounds good to me!

Most of us have no choice when paying Council Tax – but there are ways to make sure you aren’t paying too much.

Along with everything else, my Council Tax bill has gone up. For my council, it’s up by 6.4%, which works out as an extra £15 a month. This is the biggest annual hike I’ve experienced, and it adds up to £175 extra over the year.

Though I’ll be able to afford it, I know not everyone will – and some might have seen larger increases. Many councils have voted to increase by the maximum 4.99% that’s allowed, and few others have been forced by financial issues to trigger referendums for even larger hikes.

So I thought it was a good opportunity to share with you ways you might be able to pay less, or at least make how you pay work better for you.

What is Council Tax?

Your Council Tax largely pays for local services, so the amount you pay is set each year by your local council. It varies all over the country.

Some of the money will also go towards funding social care as well as police and fire services in your area.

There are eight ‘bands’ of council tax, all based upon the approximate value of the property in 1991. A is the lowest, H the highest.

You can get cashback from Santander

There are two current accounts you can open which help you save on your Council Tax bill. Though these current accounts have fees, you generally make the money back on cashback from bills, including Council Tax as long as it’s paid by Direct Debit.

The Santander Edge and Edge Up current account will give you 1% cashback on your Council Tax. The money is returned to your account along with cashback on other bills, such as energy, broadband and water. However you will pay a monthly fee.

If you already have the Santander 123 or 123 Lite accounts (now closed to new customers), then that has a lower monthly fee. You can read my comparison of the four accounts to see which I think is best.

To be fair, most of you won’t be able to cut the monthly rate unless you fit one of these exceptions:

Living alone? In which case you’re able to get a 25% discount on the rate. If you’re the only adult but have children under 18 or not in education, then you qualify for the discount too as a sole adult

Students pay nothing if they’re in full-time education

If you are unemployed or meet other conditions, it’s possible to claim Council Tax Reduction payments, which could be as much as 100%

Got a second home? You might be able to get a discount too. It’s up to the local council, but if it’s furnished it’s possible to get up to 50%. If it’s empty for two years or more, they can charge more

If someone has passed away, there is no charge for six months

Disabled people who need a bigger house to accommodate space for wheelchairs or extra bathrooms can get their band reduced down a level for example they’d pay C rates on a D property

Adults who are medically classed as having a severe mental impairment will get 100% discounted if they live alone or with others who don’t pay, 50% if you live with a carer only, and 25% if you live with just another adult

Live in carers can get a 25% to 50% discount if they meet the conditions

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

You can check to see if you’re paying too much

Use this government site (or this one in Scotland) to see what band houses around you are in. If it looks like houses around you are less, it might be worth appealing. The StreetCheck website is good to find out neighbouring postcodes.

You can also see what neighbouring houses are valued at, to help get a sense of whether yours is worth more or less. Zoopla is good for this. You’ll ideally want to see valuations from 1991 as changes could have taken place since then.

If both look good, you can try to appeal. If successful you’ll not only get a discount going forward, but also backdated payments.

Be aware though that the council could also choose to raise your band – and how much you pay (and for any neighbours who are also then found to be underpaying).

I’ve taken a look and most of the nearby houses are all on the same band, so it’s unlikely I’d be able to get it changed to a lower band.

You can pay Council Tax over 12 months if you’d prefer

Most Council Tax bills are set to be repaid over 10 months, meaning you don’t pay anything in February and March. For some this break gives a little breather after Christmas to pay off extra expenses.

I choose to spread the cost over 12 months instead of 10, so I know exactly what I’m paying each month. You need to ask your council to change this if you want to do the same.

Top paying interest, ethics and a decent switching bonus make the account worth considering again.

There’s been a revamp of the account. Not only does it offer one the highest interest rates (for some), newbies can also now get 1% cashback on spending. Plus you can nab a decent switching bonus. It also ranks well as an ethical bank and scores highly for customer service. However, the building society has ditched the large 0% overdraft.

So are these extras enough to make it your main account? Here’s what you get with the FlexDirect, and whether you should open up an account.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

What is the Nationwide FlexDirect account?

The FlexDirect account is a current account from the Nationwide Building Society. It’s free to open and use, though you do have to pay in at least £1,000 a month to get the interest. That doesn’t need to be in one go, or stay in the account.

You cannot get the account if you already have four or more Nationwide current accounts.

Unlike many competitors, Nationwide has a decent network of branches you can access across the UK, and there’s also a phone support line.

In account interest of 5%

Nationwide’s FlexDirect account is one of the few current accounts that pay interest on balances held in the main account. And it’s usually a much better rate than you’ll get in normal easy-access accounts.

You can get 5% interest on savings – which is hard to beat right now. The rate is also fixed, at 5% for the entire year.

And you can boost your earnings if you’re in a couple. You can each have an account, and then open up a joint account too, meaning you’ll earn the 5% on £4,500.

You have to pay in £1,000 every month to qualify for the interest. This can’t be from another Nationwide account.

Sounds good? Well it has its limits.

First, there is a very important rule that could be an issue – this rate is for first-time account holders only. So if you’ve had the FlexDirect account before, you won’t get the new rate, even if you open up a new account.

You also only earn money on the first £1,500. Above this you get 0%. This means if you have the full amount possible in the account for 12 months you’ll make £75.

Also the rate also only lasts for one year (after that it drops to 1%), so you will want to move your money in 12 months.

A new feature is cashback on spending with the debit card. It’s only for new customers who’ve not had a FlexDirect in the past. You also need to be paying in the same £1,000 each month to trigger this as you do the interest, though that’s a single payment for both perks, not each.

As with the 5% interest, this cashback is only for the first 12 months. It’s also capped at £5 cashback each month, so it’ll only apply to the first £500 you spend each month.

Cashback won’t be paid on gambling, crypto transactions or cash withdrawals.

FlexDirect 0% overdraft

Sadly with the addition of the 1% cashback, Nationwide has ditched the sizeable 0% overdraft that was available for the first year.

In its place there will be a £50 interest free buffer across all Nationwide accounts. Our guide to the cheapest overdrafts will help you find a larger alternative – though there aren’t many options left now.

Nationwide had an ongoing £175 incentive for bank switchers which ended 31 March 2025. It could return at any time.

The previous offer was open to new and existing customers, so if you open or upgrade to a FlexDirect account you’ll be eligible.

You can only claim the cash once on a personal account, but unlike other banks, you can get an extra bonus if you switch a joint account (there’s just one payment for both of you on this). So as a couple you could have three switching bonuses in total.

Though there’s no guarantee it’ll still be on offer in 2025, for the last two years Nationwide has offered members with an active current account and savings or mortgage product on top, a £100 ‘Fairer Share’ bonus. Here’s everything you need to know about when Nationwide last offered this free cash.

Nationwide’s app

So far so good. Now the bad. The app is one of the main reasons I moved my main banking from Nationwide to Starling a few years ago.

There have been some massive improvements, but it still falls short of the features you get from challenger banks like Monzo, Starling and Chase.

So what does it do? You can activate a couple of features to help you save. One, Impulse Saver lets you add money to your savings account from the homescreen of the app.

The other is a round-up feature, as you see with many other banks. If you turn this on a small amount of money will be transferred each time you spend. So say you spend £1.20 on your debit card, 80p will go to savings.

You’re also able to lower your contactless limit, freeze your card and block gambling transactions.

My big frustration is that you still need a card reader. Though a recent update has reduced how often this is required, including for app payments, you can’t throw it away. And it’s not clear when you will and when you won’t need it – it just says “for some other things”, which looks like could still include setting up new payees. Of course, that might not be a bad thing as it does add an extra layer of security, but it’s not something most of the other banks I use require.

You also can’t access card details, and it’s a few clicks to find and copy or share account numbers. There are also no tracking or budgeting features.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

Account ethics

Something I’ve been thinking about more over the last few years has been how the money I keep in a bank is being used. It’s not sitting in a vault, it’s being invested and loaned by the bank. And that could mean it’s used for things I really don’t agree with – from supporting arms manufacturers through to funding new oil pipelines.

If this bothers you too then Nationwide is regarded as one of the best options. A big part of this is that it’s a building society rather than a bank, which means it has to use 75% of its holdings to lend to home buyers.

That prevents it lending large amounts to unethical sources – but it also has a positive investment policies. For example your money will not be invested in fossil fuels.

Nationwide is also a mutual – meaning it’s owned by and run for the benefits of its customers (or members) rather than shareholders.

Ethical Consumer rates Nationwide ahead of all the other major banks, so it’s a good bet if you want to put your money somewhere other than low-scoring banks such as HSBC, Natwest, Barclays, Lloyds, Santander and co.

And while the top-rated current account for ethics is from Triodos, that comes with a £3 monthly fee and a more limited app, so Nationwide represent a good alternative.

Should you open a Nationwide FlexDirect account?

Andy’s Analysis

With savings rates dropping on easy access accounts, Nationwide’s FlexDirect has sprung back into contention. That 5% can be beaten, but not with a fixed rate.

The £1,500 limit for this rate will be a frustration for some (especially since the balance used to be £2,500 a few years ago), but if that’s not a worry and you want to lock in a rate it’s worth a look – for one year only though.

And the switching offer is a fantastic extra too, especially if you’re a couple who can also switch a joint account.

The app has also improved massively, though it’s not as good as the offering from digital banks Monzo, Starling or Chase.

The cashback might sounds good, but it is limited by the £5 monthly cap – and it’s only for one year. You can beat this with a credit card like the American Express Nectar.

But, vitally in my opinion, it’s a great account to go for if you’re concerned about how your money will be invested.

What do customers say?

Customer reviews on our sister site Smart Money People rate the FlexDirect account at 4.24 out of 5, liking the customer service and the availability of high street branches. The app is where people think it could do better.

Nationwide Flex Direct summary

Cashback

1% cashback on spending for the first year (capped at £500)

Interest

5% AER (fixed) interest on the first £1,500 saved for 12 months (drop to 0.25% after a year)

Access to 6.5% AER (variable) Flex regular saver (max £200 a month)

Overdraft

£50 0% buffer

Fee

None

Requirements

Pay in £1,000 a month

Multiple accounts?

Two – one personal and one joint

Notes

Transfers in from other Nationwide accounts don’t count towards the £1,000

You’re likely paying hundreds of pounds too much on your mobile phone.

For the first 12 years of having a phone, I followed the same pattern. A two year contract with a shiny new handset, which was then renewed with an upgraded phone, and then repeated when each contract ended.

But a decade ago I switched things up. I moved my tariff to a new network, and bought a new handset direct from Apple. Since then I’ve moved between networks on a regular basis and bought and sold new handsets. And saved a ton of cash.

And you can do it too: from going SIM-only through to downsizing your data, there’s no reason you should be paying more than £8 to £10 a month. Here’s how you can save on your mobile phone contract.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

Split your handset and your tariff

Go SIM-only

The best prices are often with SIM-only deals. Here you keep your old handset or buy a new one separately and pay just for your minutes, texts and data. Since you aren’t paying for a new phone, the monthly costs are also considerably less.

You can get contracts that run from 30 days to a year, giving you far more flexibility than the 18, 24 and even 36-month deals you’re tied to with handsets (though longer SIM-only deals are still available).

At the time of writing you should be able to get a more than adequate data allowance from the major networks for under £8, and potentially as low as £5 for networks offering 5GB. And that’s before you factor in cashback or other offers.

Don’t get your handset via your network

Once you go SIM-only you’re no longer caught in that bi-annual cycle of getting a new phone when you don’t really need to. Ideally you’ll keep your handset for more three or four years. But with poor batteries, broken screens and ‘depreciated’ operating software (when updates are no longer supported on older phones), we all need to upgrade at some point.

However, you should generally avoid getting one as part of your contract. Most networks will charge you a premium on top of the handset price to get a new phone bundled with your SIM.

It’s very rare for these deals to work out cheaper, particularly for the latest handsets. Instead, you’ll save money buying it outright from Apple, Samsung or the likes of John Lewis.

Of course, the high cost of these handsets can be a barrier, but even then you don’t need to resort to including it in a contract. Apple and Samsung often offer 0% finance for two years, while you could choose a 0% purchase credit card instead. Do check your credit score first though.

Don’t forget to sell your old handset too. There are a number of sites that’ll give you a fixed amount, or you can hope for a better price via sites like eBay. Here’s more on selling old phones.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

Choosing your new phone tariff

Whether you stick to a combined phone and SIM deal or split them up, you can still bring down the cost.

Don’t pay for more data than you’ll actually use

One of the biggest ways we waste money on our mobiles is via upselling, and now the networks are all about getting us to pay for more data than we need.

A few years ago when I haggled a new SIM-only contract with Three, the salesperson said “It’s only £3 more for 20GB”. Sounds good. Except I didn’t need 20GB. I didn’t really need the 12GB I had (but that was bizarrely cheaper than the 5GB option).

And I see this upselling all the time. There are always a number of promotions offering unlimited data at what looks like fantastic prices. But you really don’t need unlimited data, so however good the price, you’re still overpaying.

Most of you will be fine with 5GB or 6GB, perhaps less, while heavier users are still likely fine with under 12GB. And that’s assuming you can’t connect to wifi at home or work to use data even less. It’s easy to check your usage history via your account. So far this year I’ve used between 5.3 and 6.57 GB each month – and the latter was when I was on holiday!

Saying that, those who also get broadband with Virgin Media should take a look at O2 as you’ll get double data, worldwide roaming and double internet speeds via an offer called Volt. Just make sure you’re getting a decent price on each service.

Don’t just stick to the big companies

You’ll have spotted that most of the cheap deals are with smaller networks. And I bet you’re warry of switching in case you can’t get reception.

Well, there are actually only four different phone networks – O2, EE, Three and Vodafone. All the others “piggyback” on one of these. So, for example, Giffgaff runs on O2 and Lycamobile uses EE.

This means you get exactly the same reception as someone on the host network but at a far lower price. The only real difference will be in customer service, though you’ll also lose network-specific benefits from the big brands, such as O2 Priority Moments.

I’ve written in more detail about these so-called ‘virtual mobile networks‘, including which ones operate on which main network.

It’s also relatively easy to bring your number with you. My moves across different networks all took less than 24 hours though it might take longer if weekends or bank holiday get in the way. Just ask for a PAC number, which you can get just by texting your network.

Text INFO to 85075 and you’ll receive a message from your network outlining if you in our out of contract. If you are still locked in you’ll also be told how much it’d cost to end the deal early.

Make a note of this date, and you can usually negotiate with your network up to 30 days before the end of a contract. This gives you the chance to see if you can get a better deal with your current network, and if not start the process of moving to a cheaper one.

But if you’re already passed that minimum term, you’re free to hunt for a new deal.

Compare prices

Just as you would with your gas or broadband, it’s important to see what other networks are offering. MoneySupermarket or Uswitch are decent price comparison sites, though they don’t include all the SIM-only networks.

You’ll also often find lower prices for the big networks via these sites, allowing you to access some (though not all) of the freebies available by those companies.

Check for cashback

If you’re switching network or upgrading without a new handset there’s less of a chance for cashback, but it’s worth checking anyway. Try both Topcashback and Quidco for SIM only too. And if you’ve never used cashback sites don’t forget the new member bonuses to get even more back!

You can also earn cashback to knock more off your bill using the app Airtime, but only with the major networks and a handful of others.

Call your network to see if they’ll negotiate

It’s still worth calling your network to see if they can match or beat the total savings you’ll find from the tips above. It helps to do some research first so you know what you can get if you switch.

Then ask to be put through to the ‘terminations’ or ‘disconnection’ team as they’ll usually have more sway. You can even do this over live chat if you prefer.

I did this the most years with Three. I either had my price knocked down or data added for the same price, beating what I’d get elsewhere. None of these deals were available on the Three website, but came from saying I wanted my PAC.

A warning here though. You will be starting a new contract if you do this, which will overwrite pre-existing offers such as free roaming with some networks.

Gift cards are a popular present option, but they have some major downsides.

From birthday and Christmas through to leaving and wedding gifts, at some point, we’ve all received and purchased gift cards. It makes sense – they’re an easy choice when you don’t know what to buy someone. The issue is that every time you buy a gift card you risk losing the cash on it.

The majority of the time you’ll be fine, but there are a few risks of gift cards, many of which can be reduced or avoided. Still, to be safe you need to know the good and bad of gift cards.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

When gift cards are bad

I’ll lead with the dangers of gift cards – the reasons you could find your gift card is wasted cash.

Gift cards prevent you shopping around

One of the key tenets of Being Clever With Your Cash is getting the best deal. The easiest way to do this is very simple – shop around for the best price.

Yet if you have a gift card to use at Shop A, but the best price for what you want is at Shop B, you’ve no choice but to buy it from Shop A.

Ok, so it’s not the end of the world if we’re talking about a few quid, but you won’t want to miss out on larger savings.

And what if the shop you have a gift card for doesn’t have anything you want? You’ll end up using it to buy something you don’t need and probably won’t use. It’s a waste of money.

Refunds go back to a gift card

Another big risk of buying with a gift card becomes apparent if you need to return your purchase.

The money will go back to a gift card for the same shop. This is less of an issue if you shop frequently at the retailer, but what if it’s a one-off purchase?

It’s particularly bad if it’s a large purchase leaving hundreds of quid on a gift card rather than in your bank account.

This is why I never purchase discounted gift cards for anything I’m not certain about.

You also need to be careful here that you don’t chuck out your gift cards once you’ve used them. While most retailers will issue a new gift card, some will require the funds to go back to the original card.

Be aware that online purchases could also be refunded to credit that can only be used online. John Lewis is one worth highlighting here.

Say you’ve got a paper or plastic gift card you can use at both John Lewis & Waitrose shops and websites. Use it on the John Lewis website and any refunds are in credit just to use online only at John Lewis – but not Waitrose.

They often have hidden expiration dates

Most gift cards will have an expiration date. If you don’t use them before this date you lose the cash. That’s fine with paper vouchers, and most sent by email, where you can see this date in black and white.

But you need to be particularly careful with plastic gift cards. These can be loaded with different amounts at purchase, which means the details printed on them are often generic.

This makes it hard to see when the card expires, or how much is left on them. This means that a huge number will expire unused.

There are also different rules for different cards. Sometimes they’ll be valid for a set period, perhaps one or two years. Others will be valid for a certain time since they were last used. But it’s not always clear which is which.

Some, such as the One4All card will start charging you a monthly fee after a certain time (with One4All it’s 90p per month after 18 months).

The best way to prevent them from expiring (other than using them straight away) is to make a note of when you bought/received the card and its value. Then each time you use it, make a note of the date and new value, or keep your receipts with it, they typically have details of what’s left on the card.

Often you’ll find that if you don’t use the gift card in one go you’ll be left with a few quid, or even pennies, left over. They’re not enough to buy something outright, so you keep hold of the card until you next go to that retailer.

And then you forget. And that money sits there until the card expires. More wasted money.

There can be limits on using multiple cards

If you’re asking multiple people to give you cards to go towards a purchase, check if there’s a limit to how many cards you can use in a single transaction.

Marks & Spencer and Curry’s, for example, will only allow 10 to be used at once.

There’s no protection with a gift card

Spending with a credit or debit card can give you some advantages over gift cards. Section 75 of the Consumer Credit Act protects credit card purchases over £100, while the Chargeback scheme for credit and debit cards is a route if you’ve problems with purchases under £100.

If you pay with gift cards, or cash for that matter, you lose this protection.

And much like cash, if you lose your gift card there’s no way of getting it back. So try not to carry too many gift cards around with you.

They can be worthless if the shop goes bust

We’ve seen a succession of high street staples shut their doors over the last few years, and when this happens the administrators don’t have to honour any gift cards.

Often shops closing down just stop accepting outstanding cards. Jessops, HMV and Peacocks all made gift cards and vouchers worthless overnight when they entered administration.

It’s also unlikely that buying gift cards on a credit card and using Section 75 would help you get your money back in these situations as gift card balances are usually far less than £100.

If, despite this, you still want to give a card, it would be wise to avoid any retailer which appears to be struggling.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

When gift cards are good

That’s one long list of negatives when it comes to gift cards… but there are a handful of times when they can be worth the risk.

When you get an extra discount

You don’t have to buy them as gifts – you can buy them for yourself for your own shopping. And that can be a good thing when you’re able to buy discounted gift cards.

It could mean you pay less for your everyday shopping, including at places where it’s hard to find offers. For instance, though small you could get 2% back at Amazon or 4% at the supermarket – better than the rate you’ll get from a cashback credit or debit card.

And since the gift cards are like cash, you can stack them with other promotions and savings, such as in tandem with Meerkat Movies at the cinema, or with BOGOF offers.

For example, I often get an extra 6% off John Lewis gift vouchers via my Scottish Friendly ISA perks. It comes as an email but I print it out and I’m able to use it both online and in-person at the department store and in Waitrose.

Supermarkets often run promotions on selected gift cards, such as Spotify, Pizza Express, Cineworld and Footlocker. If we spot decent deals we’ll share them on our gift card deals page.

When you spend them straight away

The main way to avoid the bulk of risks outlined above is to spend your gift card as soon as you get it! That way they can’t expire, be lost or lose their value of the shop goes bust.

When you can use them on lots of things

If you’re set on buying a gift card for someone then you could look at one you can use at multiple retailers.

Though there’s always the risk that the companies selling these could go out of business themselves, you’ve got a choice where you shop. The main ones are One4All and Love2Shop.

Our podcast

Listen to Cash Chats, our award-winning podcast, presented by Steve Alderton and Editor James Andrews.

Really you’re better off giving cash, sending a cheque or transferring money to a bank account. Yes these can feel lazy and seem impersonal. But really, is that very different from a gift card?

I know people worry that the money will just disappear from a bank account on everyday spending than buy something special. That certainly is a risk, but you can steer someone to use the gifted money in a certain way.

Perhaps you can say “use this for a nice meal out”. Or to “put it towards a new winter coat”. Hopefully if you suggest this you’ll get a nice text or email sharing when and where it is spent.

And don’t be put off sending a cheque (if you’re still got a chequebook). There are a number of banks now that let you pay in a cheque via the app.

Prices are changing all the time, usually upwards, and the rate these changes are measured is generally called inflation. However there are a few different options here, so we’ve broken down what they all mean, and why they matter.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

What is inflation?

Inflation is a measurement that helps us track the price increase of goods and services over time.

It compares the cost of things today with how much they cost a year ago. And the average increase in prices is what we call the inflation rate.

Let’s take a loaf of bread as an example. If it costs £1 to buy a loaf today and next year it costs £1.10, the annual inflation for that loaf of bread is 10%.

And falling inflation doesn’t mean prices will go down. If a rate moves from 5% to 4% month on month prices are still increasing, they’re just doing so at a slightly slower rate.

What is deflation?

Deflation works the opposite way and tracks the rate that prices decrease for goods and services over time.

So looking at that loaf of bread again. If it costs £1 to buy a loaf today but that falls to 90p next year, then the deflation rate would be -10%.

What’s the latest inflation rate?

Inflation is measured over a 12 month period, with the latest figures announced in the middle of each month. You can find out current rates in our UK Inflation: what is the current rate? article.

How is UK inflation measured?

The Office for National Statistics (ONS) is in charge of measuring inflation in the UK and publishes figures each month to show how prices have changed.

There are three common measures of inflation; Consumer Prices Index (CPI), Consumer Prices Index with Housing (CPIH) and the Retail Price Index (RPI).

This can get a little confusing at first with all of the different figures, but the breakdown below shows how each one works and how relevant it is to you.

CPI inflation

The Consumer Price Index (CPI) is the UK’s official measure of inflation and the rate you’re likely to see make headlines.

For CPI, the ONS tracks around 180,000 prices of 700 hundred everyday items in an imaginary shopping basket (called the basket of goods) to work out the inflation rate.

These everyday items and services fall into one of the following categories:

Food & non-alcoholic beverages

Alcohol & tobacco

Clothing & footwear

Housing & household services

Furniture & household goods

Health

Transport

Communication

Recreation & culture

Education

Restaurants & hotels

Miscellaneous goods & services

The basket of goods gets reviewed each year to make sure that it gives an accurate picture of how price rises relate to our spending habits and patterns.

This means that products and services might get added to the basket each month, while others are taken out.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

What is core inflation?

Another measurement for inflation you may have come across is “core inflation.” Core inflation tracks the same goods and services as CPI but doesn’t include food, energy, alcohol and tobacco.

These are taken out as they’re generally seen as the most volatile, so core inflation should give us a better understanding of how prices are changing outside of the everyday essentials.

What’s in the basket of goods?

Inflation in the UK is measured by looking at the price changes for an imaginary shopping basket, known as the “basket of goods.”

The basket includes lots of products and services that we use and tends to change to reflect our spending habits to make sure that the inflation rate is relevant.

The contents are refreshed each year, and in March 2024, 16 were added to the basket including air fryers, vinyl music and gluten free bread. Items that have been taken out of the basket include hand gel, rotisserie chicken and bakeware.

CPIH is a measure of UK inflation that takes into account housing costs, as well as everyday goods and services.

It uses the same basket of goods as CPI but also includes prices for things like the cost of owning, renting or maintaining your home. It also takes into account expenses like council tax.

CPIH is the newest measure of inflation and was introduced in 2013 to plug some of the gaps left by CPI (mainly the lack of tracking of housing costs.)

RPI inflation

RPI used to be the main measure of inflation in the UK until it was replaced by CPI in 2011.

It tracks the same basket of goods currently used for CPI but also includes things like estate agent fees, buildings insurance, TV licence and mortgage interest payments (which aren’t included anymore!) And, it tends to be higher than the CPI and CPIH measure of inflation.

Although RPI isn’t the main inflation figure anymore, it’s still used to set the price of things like interest on student loan repayments and rail fare increases we get each year – though there is the flexibility from the government to pick a lower rate if RPI is significantly high.

RPI also plays a big role in the level of retirement income people get from final salary pensions and annuities.

So you might be wondering why we still use RPI if it’s technically been replaced. Well, there’s an ongoing debate about its purpose and relevance.

On one hand, final salary pension schemes and annuities may see less of an income boost if RPI was scrapped altogether.

However, the government’s use of RPI compared to CPI, in particular, has also come under fire.

Usually, the government links its own spending – which includes things like the state pension, statutory sick pay and benefits – to the CPI rate of inflation, which is lower.

However, it uses RPI (which is higher) when it comes to the costs we pay such as train tickets, car tax and student loan interest to name a few.

At this stage, it remains to be seen what will happen with RPI and whether it is replaced completely by one of the other inflation measures.

Our podcast

Listen to Cash Chats, our award-winning podcast, presented by Steve Alderton and Editor James Andrews.

Inflation shows how much the cost of living is rising and gives you an idea of your spending power. So, the higher the rate of inflation, the more expensive everyday expenses tend to be.

With the current cost of living crisis, we’ve all seen how sharply prices have risen over recent years. From eye-watering grocery bills to the cost of heating and powering our homes, prices have risen across the board.

High inflation has also caused significant increases to the interest base rate by the BoE. That’s because the BoE raises interest rates in an attempt to bring down inflation to its 2% target. And changes to interest rates can impact both borrowing (especially mortgage) and savings.

Inflation also increases the risk of your money losing value in real terms. One area is wages. If they don’t increase in line with inflation you’ll need to use a higher proportion of your income to buy the same goods and services.

Similarly, your savings could lose value as well because, if your money is earning less interest than the rate of inflation – you won’t be able to buy as much with it.

Save money on beer from the likes of Brewdog, Beer52 and more.

This page is dedicated to special offers, sales and vouchers which will help you get already cheaper beers for less, or make rarer and more expensive small-batch beers more affordable.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

Free beer

Free 4-pack of Beavertown for Londoners (ended)

You can currently get a free four-pack of Beavertown Satellite Super Session IPA. All you’ve got to do is sign up, purchase a pack from a London Co-op and upload your receipt using the link you’ll have been sent to claim the money back. You can get up to £7 for a 4-pack.

This offer ends on 30 November 2024 or when 3,600 cashback redemptions have been made.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

Beer 52

Beer52 is a monthly subscription box full of beers and there are always deals out there to save on your first box. Alternatively you can also buy individual beer as you please via an online beer shop.

Also, from time to time Beer52 also offer heavily discounted boxes of beers that are close to or just past the best before date. They’re still good to drink, and I once picked up a fantastic Stone Brewery box with 8 beers for about £12. I’ll add any of these deals I spot below.

If you don’t want to keep getting beers in subsequent months, which will be charged at the full price, you’ll need to cancel. You can choose to take holidays if you’d rather where you miss the odd month.

£5 back when you spend £15 at small shops won’t be returning

Every year, American Express ran a Shop Small offer giving money back for every £15 spent at small businesses. You could get money back from shops, restaurants, pubs and even places like hairdressers, galleries and dentists in the form of a statement credit.

But from 2024 it didn’t return. Here’s everything you need to know.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

What happened to Amex Shop Small in 2024?

One of my favourite perks for being an American Express customer was always Shop Small. You’d spend a set amount (around £15) and get a fiver back. It encouraged you to support local businesses and make some money!

However in the last years of the offer, it got smaller and smaller, reducing how many times you could use the promotion and how long the offer ran for. Eventually it was just three times over just three days – a far cry from the two weeks and ten redemptions previously.

Well, American Express quietly killed it off completely in 2024. Their press office told me that a competition announced in October 2024 was instead of the cardholder credit offer, rather than as well as.

Cardholders nominated their favourite independent retailers. There were 50 cardholders who won £1,000 credited to their card. You could enter ten times until 7 December 2024, though it had to be a different shop for each nomination.

In addition, ten of the nominated small shops got a £10,000 grant.

We don’t yet know whether this competition will return for 2025.

When is Amex Shop Small 2025?

American Express won’t be running the scheme in 2025.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

How Shop Small 2023 worked

Though it won’t be back this year, here’s how it last ran in 2023.

The pretty big change was a reduction in how many times you could use the offer.

Earned £5 back for a spend of £15 or more (before 2021 this was £5 for every £10 spent)

You could get the offer at up to three different small shops (previously five shops in 2021 and 2022, and before that in ten shops)

There was a cap of £15 earned per card (previously £25 in the last two years, and £50 before that)

It also lasted for just three days. THREE. This reduction was a huge difference to previous years. In 2022 it lasted for ten days, down on the 13 of winter 2021, and 16 days in the years before this.

Other conditions stayed the same, including the rule that you could only earn a Shop Small credit once per retailer, per card.

Here’s how you could take advantage of the offer when it was running. Note the following all refers to the offer as it ran in 2023.

Add the offer to your card

The offer wasn’t automatically applied to your account. You needed to “add” the offer to your card to take advantage.

Throughout the year you also saw other decent offers. Over the years I gained £250 off a £500 United flight, £20 back from a Eurostar trip, 10% off LNER bookings and £100 back from a £250 hotel booking spend – and there were plenty more. I reckon I easily made another £50 to £100 each year from these offers, sometimes much more.

Add it to your partner’s card

If you had an additional, or ‘supplementary’ card on your account for your partner, then they could also add the offer to their card.

This meant you could both take advantage of the promotion, and you could shop twice at the same retailer – once with each card.

Apply for an extra American Express credit card

You weren’t limited to a single American Express card. Since the offer was per card not per person, if you got another card or two in your name it increased the retailers you could spend at.

It’s easy to always buy things at the same big shops, or visit the same places. This was a chance to try new stores and businesses.

Some of the businesses I looked out for were:

Off-licences

Corner shops

Cafes and restaurants

Bars and pubs

Small boutiques

Museums and galleries

Services like dentists, dry cleaning or picture framing

Buy gift cards

If there was nothing you wanted to buy in the moment but you knew there would be purchases you’d make at specific businesses in the short term, then you could buy a gift card using Shop Small.

Split the bill

If you used Shop Small at a restaurant and you were with someone else using Amex, you could split the bill so you both got the credit.

Who paid for Amex Shop Small discounts?

The money all came from American Express. The shops and retailers weren’t be out of pocket at all. You genuinely were helping shops by using this offer which is why it’s such a shame it’s gone.

Our podcast

Listen to Cash Chats, our award-winning podcast, presented by Steve Alderton and Editor James Andrews.

The changes to the promo in 2021 changed how I took advantage, and that was even more so with the latest cuts in 2023. I used to mainly spend in restaurants and bars, using it as an opportunity to enjoy a meal out with a little discount, but that got harder over a weekend, especially over multiple cards.

So I looked out for retailers that sold gift cards. This meant I could extend the offer by a few weeks and months.

How to get an Amex credit card

It could take up to two weeks for your card to arrive, though it’s usually much quicker.

(A quick aside, if you don’t feel confident you’ll be able to pay off your spending every month, then don’t even apply! The interest charges will far outweigh the benefits you get).

Right now there are a couple of boosted refer-a-friend welcome bonuses, which is normally a great extra. You can get the increased deals via:

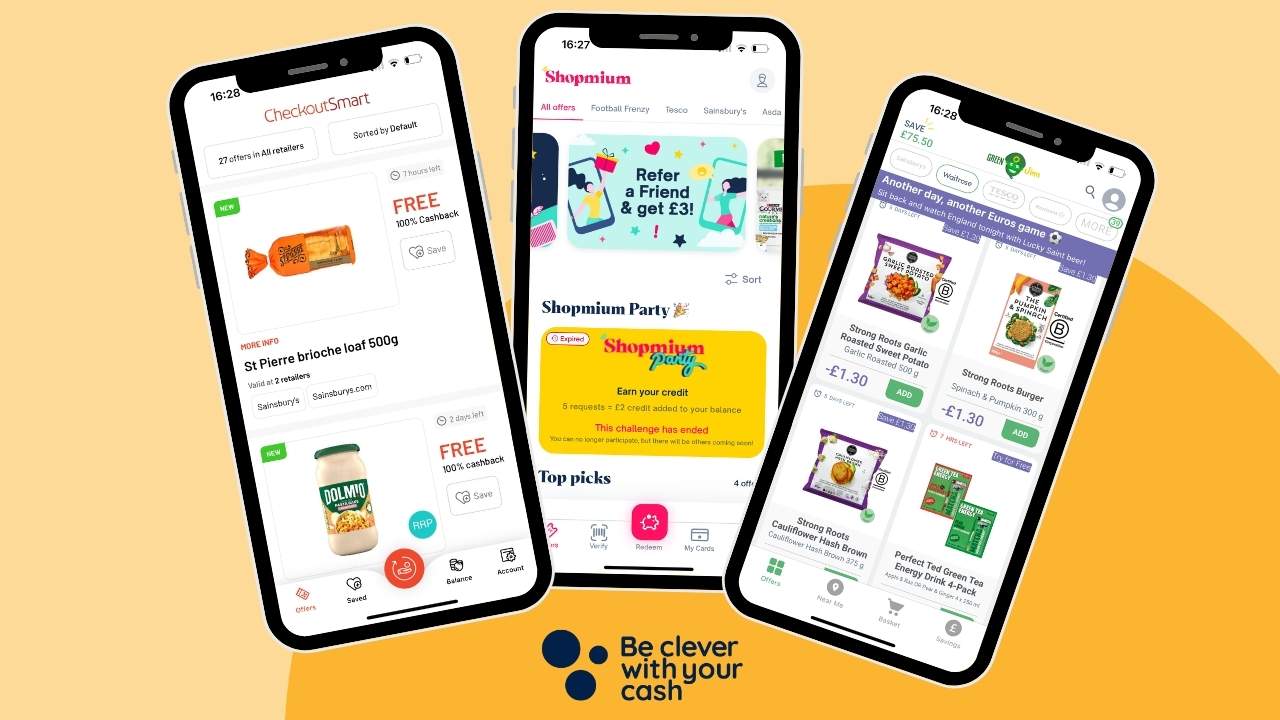

Just how good are the deals on grocery cashback apps?

We’ve reviewed CheckoutSmart, Shopmium and Green Jinn to see just what kind of savings these apps are giving and whether it is worth using them.

From money off to free products, we’ll let you know whether they are worth checking out. Plus there’s a code to get a free treat with Shopmium!

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Paid advertisement

How supermarket cashback apps work

Unlike when you use cashback sites to shop by clicking through, here the cashback is earned after you’ve bought the goods.

You need to look at the apps before you head to the supermarket – or even when you’re walking the aisles – to see the different promotions, pick up the products as you shop as normal and then claim your cashback when you get home.

Each app works slightly differently, but they all require you to select the offer you are claiming and upload a photo of your receipt.

If that’s all done correctly you’ll start to build up a little bit of extra money which you then transfer to your Paypal or bank account or even transfer for e-vouchers.

Most of the time it’s a proportion of the item cost you’ll get back, but you can sometimes get all your money back – making the items free.

The majority of the products listed on these apps are new. That’s because brands want you to try something different, hoping you’ll keep on buying it but you will occasionally see everyday products.

By the way, they work with online orders too, and you usually don’t need to print out the receipt. Just take a screengrab of it on your phone or download it as a file.

Supermarket cashback apps compared

There are currently three different apps we know of and to be fair that’s probably plenty, as it does take some preparation before you shop to get the most out of them.

Shopmium

Main supermarkets on the app

Tesco, Asda, Sainsbury’s, Waitrose, Morrisons and Co-op

Other retailers (depending on products)

You’ll sometimes see offers for Iceland, Ocado, Boots, WH Smiths and others

Minimum payout level

£10 through bank transfer of PayPal

Welcome offer

Use code KHMYEEFW for free Cadbury Buttons

Referral scheme

£3 for every friend you refer who claims cashback

Having recently changed their payout minimum to £10, this may be a negative for some, but due to the number of high paying offers on this app, it is relatively quick to reach the £10 threshold and therefore it is my top supermarket cashback app.

That said, it does have some negatives. You have to click on each product to see what the offer is, which can be time consuming and not the easiest thing to do whilst you’re shopping.

Watch out too for products where different versions are on offer at different supermarkets. Again you need to click in to check.

Therefore this app is one that requires a little of your time before you shop. You can, however, filter the selection to a specific supermarket so you know what offers apply where.

Saying that it offers plenty of high paying cashback. This month for example you can try Domestos spray for £1 so that’s £2 cashback on your purchase and Comfort for £1, so again around £2 back in cashback. It doesn’t appear to offer many ‘free’ products where you get the entire cashback but more offers such as 50% off, or ‘try for £1’ or save £1.50.

You can make extra cashback with special tasks such as submitting a specific number of cashback requests within a certain timeframe. They also offer a loyalty scheme where you can progress through the tiers to get extra benefits such as exclusive offers and birthday treats.

CheckoutSmart

Main supermarkets on the app

Tesco, Asda, Sainsbury’s, Waitrose, Morrisons and Ocado

Other retailers (depending on products)

Iceland, Co-op, plus many more although most don’t have any offers apart from the daily £10 draw

Minimum payout level

£1+ for your first payment; £5+ thereafter. NB payments under £20 made to bank or PayPal will incur a 5% transfer fee. Payments to e-vouchers just have to meet minimum payment level of £5.

Welcome offer

No

Referral scheme

No

CheckoutSmart tends to be the best for freebies. It also has a far wider list of supermarkets that are easy to filter.

In terms of ease of use you can see the product and what the discount is at a glance, helping you see whether it’s worth your time and also allowing you to check this app whilst you’re shopping.

You can also filter the offers in terms of the highest percentage paid, which will give you the free products (100% cashback) first. The free products may be good enough to entice you to another supermarket. At the time of writing there are free energy drinks, salami and chicken bites available at different retailers.

If you want cash to your bank account or PayPal the app has a high £20 payout level, though freebies can help you reach that amount if you use the app frequently. Or you can instead choose a gift card, though only in multiples of £5. This payment method is set to alternate each week with the cash payout. The payout time can take a long time and I’ve often waited over a week to receive my payment.

There is a negative with this app, in that there are times where there is little change in the offers available and some offers seem to have been on the app for ages. You can also find that this app may have some retailers with very few offers available at times – I often find Morrisons lacking in new offers for example.

Share a particular coupon with friends (marked with a green tab) and if they redeem it you’ll get a bonus £1

Green Jinn is easy to use and you can quickly select your retailer and see what offers are available without having to click into an advert like you do with Shopmium. There are some different products from what you see on the other apps as it claims to only offer good quality or healthy food and drink. At present, you’ll find lots of cereal bars, natural energy drinks and healthier drinks such as kombucha.

There are some really good offers for free products and some high-paying cashback offers too. It’s nice to be able to try a product for free or for £1 for example, that you may not have picked up usually. Just last week, I got cashback for the full price of a 4 pack of matcha fizzy drinks – that’s a £6 item I got to try for free!

Underneath all the offers is a section for each supermarket labelled ‘your everyday shop’ where you’ll usually find two cashback offers on fruit or veg so don’t forget to scroll down to these.

This app also offers a variety of cashback on products at Boots and WH Smith including non-food options such as Rock Face deodorant which you can currently try for £1 from Boots.

The only gripe I have with this app is that since the products are quite niche, they’re often hard to locate. There’s been some really interesting CBD drinks to try for free at Waitrose, but I’ve been to two stores and have yet to find them!

Get cashback on all your supermarket shopping

Don’t forget you can use apps like HyperJar, Cheddar and JamDoughnut to buy supermarket gift cards and earn cashback. So, say you earn 4% back on a £100 Tesco gift card, that’s £4 off your spend! Here’s more on each app;

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

What to watch out for

Cashing out your cashback

When Shopitize suddenly closed a few years ago, many customers lost money that they hadn’t withdrawn from the app. So it’s vital that you don’t let money build up with these apps.

Payout limits are something to watch out for. It can take a while to reach the cashback threshold in your account to let you cash out – a particular issue with CheckoutSmart.

All three apps require you to request to cash out as none offer an automatic option, so you have to remember to do it.

Spending money to save money

Just as important is to not let the discount convince you to buy something you don’t want – just because you’re saving 50p, it doesn’t mean you should buy it. But that said, if an item is free, it’s worth giving it a try or even donating it to a food bank if you’re’ not likely to consume it.

I personally love the option it gives me to try something for a discount price or even free that I wouldn’t normally buy but I’m never encouraged to try something new if the cashback offered is really low.

Uploading errors

Frustratingly, receipts will sometimes be rejected for quality purposes. You then need to retake the photos and upload them until they are accepted. But this is rare, and even receipts that have been crumpled up in my shopping bag have been accepted.

And obviously you need to remember to print the receipt at the supermarket too. And don’t forget to hold on to it until your cashback claim has been accepted – usually a couple of hours to a day at most.

Buying the wrong products

Not all offers are valid at all supermarkets, and products can be very specific in terms of size and flavour. This means there’s a risk that you accidentally pick up the wrong product or buy it at the wrong supermarket.

I’ve certainly missed out by accidentally picking up raspberry rather than strawberry jam, or bought in Tesco to find the offer was only valid for Sainsbury’s.

You might also find that one flavour is on offer from one shop, and a different flavour from another, so read the full offer details to check.

While you’re at it, double-check the terms of the deal too. Rather than a simple money-back promo, or it could be along the lines of buy one get one free.

Finding the items in-store

And I wouldn’t go out of your way to visit a supermarket for one of these offers. I’ve often been frustrated to find my local branch didn’t stock the item.

It’s best to treat it as something to check when you get to the supermarket, rather than plan your shopping around it.

Are supermarket cashback apps worth using?

Since uploading a receipt and scanning the barcodes doesn’t take that long (maybe two minutes max) I’d say it’s worth the time to get cashback on a variety of products.

It is worth checking all three apps before you go shopping or even when you’re walking from the car to the supermarket entrance, to see if there are any products with a good cashback offer that may be worth keeping an eye out for.

Remember that not all offers are valid at all supermarkets, and products can be very specific in terms of size and flavour, so make sure you’re picking up the right product at the right supermarket.

And keep an eye out for products that are on offer at the supermarket. Green Jinn and CheckoutSmart allow you in theory to get double discount, so you could end up getting cashback on the rrp whilst the product is on offer at the supermarket – in theory making you some extra money. This doesn’t work with Shopmium though.

All in all, I’m a fan of using all three apps, but I’m willing to spend an extra five minutes before or during my weekly shop to see what offers are available and to take the time to claim the cashback once I’m home. The fact I can sometimes try items for free, makes it worth the effort.

Featured switching deal

Featured switching deal