This cash hack will help you save regularly at big brands including John Lewis, Tesco and Odeon.

Some of you will get access to all sorts of deals and discounts via your employer (if you’re not sure – ask your HR department!) or membership of something like health insurance. These work perk benefits can be pretty good, often giving money off gift cards and cheap cinema tickets.

I’ve had access to different ones in the past from working at the BBC, having BUPA health insurance, and a Scottish Friendly ISA. But what if you won’t work for a company with a scheme, or can’t afford things like BUPA?

How anyone can get access to a “work perks” scheme

I’ve found a way that’ll get you access to one of these schemes – and there’s no need to change your job, or sign up to insurance with a high monthly fee in order to get these discounts.

Instead the trick shouldn’t cost you anything. In fact it’s possible that you could make around £150 on top (more on this in a bit).

These deals are available via an investment company called Scottish Friendly, and to get them you are required to open an ISA and invest money.

There’s obviously a risk with Investment ISAs that you could lose a little bit of money – investments go up and go down. Plus you can only open and pay into one of these accounts each year. More on this further down the page.

First though, a little about the types of discount you’ll get so you can decide if it’s worth it.

What you get with from Scottish Friendly’s perk scheme

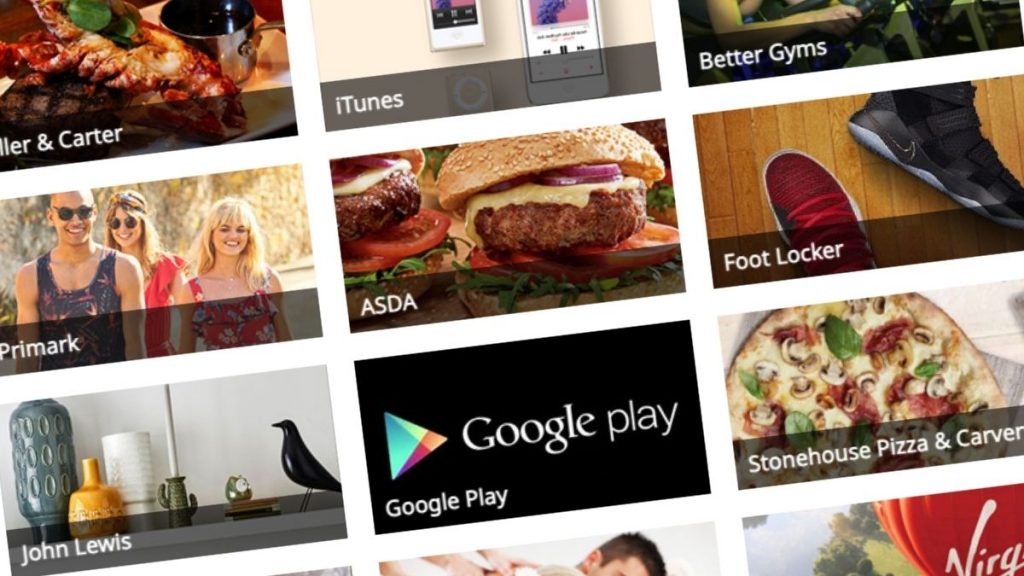

Discounted gift cards

The gift cards you get can be physical or digital. Some are reloadable, so once you’ve got the first one it’s easy to add more money one. Though gift cards have risks, use them right and you can stack them with other offers as they’re treated as if they were cash. At the moment the offers include:

- 5.5% off John Lewis or Waitrose

- 4% off Asda

- 4% off Morrisons

- 5% off Sainsbury’s

- 4% off Tesco

- 6.5% off M&S

- 4% off Uber

- 3% off Ikea

- 6.5% off Argos

- 7.5% off Asos

- 5.5% off Primark

- 4% off Wickes

- 9.5% off H&M

- 13.5% off Sky Store

- 7.5% off Curry’s

- 4.5% off B&Q

- 8.5% off Body Shop

- 6.5% off Ticketmaster

- 6% off Pizza Express

- 9.5% off One 4 All cards (which you can spend at places such as John Lewis)

- 9.5% off Pizza Hut

- 9.5% off All Bar One and other Mitchel and Butler pubs

All correct at the time of writing.

Cheap cinema tickets

Membership also gives you discounted cinema tickets. Obviously cinemas haven’t reopened yet, so these deals aren’t running, but are worth considering when they do.

You can get 2D tickets from all the big chains. Whether it’s cheaper than other similar schemes, such as Tastecard or Kids Pass does depend on the chain and location you pick. And you might be able to save money via these other deals. Even so, it’s a good option to have on hand.

Some chains also allow you to upgrade to 3D or premium seats, or save on your snacks in advance. You can also save on annual memberships. These are actually pretty good savings. A year of Cineworld Unlimited (outside Central London) is 23% less than full price, and a year of Odeon Limitless (also outside London) is 27% less.

Chains include

- Empire

- The Light

- Merlin

- Odeon

- Showcase

- Vue

Other entertainment discounts

Though paused due to the pandemic, there are also discounts for theme parks such as Alton Towers and Thorpe Park, experiences such as the London Eye and Go Ape, and memberships to things like National Trust.

Money off in restaurants

You’ll get a card you can flash at various restaurants for money off, including the following:

- 3.5% off Uber Eats or Deliveroo

- 9.5% off at Costa

- 10% off at Tortilla

- 20% off at Carluccio’s

- 20% off at Frankie & Bennies

- 25% off at Prezzo

All correct at the time of writing.

How to get these discounts

Open up an ISA

You’ll need to open up an Investment ISA with Scottish Friendly to get the rewards.

Deposits start from £10 a month. You can stop these at any time, and keep the ISA open even with no money left it in – which should mean you keep access to your perks and discounts.

There are fees attached, so your money could be worth less when you take it out than when you put it in. But they could also have grown.

It’s really important to point out that you can’t pay into more than one investment ISA in a financial year. So if you’ve already done this in 2021/2021, you’ll need to wait until April 6th 2022.

And either way, by following this trick it does prevent you from paying into another investment ISA in the 21/220 financial year. You’ll be able to pay into a different type of ISA, such as a Cash ISA, or Lifetime ISA.

So you need to be sure that you wouldn’t rather shop around for a different investment ISA.

Get your welcome bonus

With the My Easy Choice ISA you can also get a gift card reward when you go direct, starting at £15 up to £45, depending on how much you deposit. It’s an easy win.

- If you deposit £10 to £14.99 a month you’ll get a £15 voucher

- If you deposit £15 to £19.99 a month you’ll get a £20 voucher

- If you deposit £20 to £24.99 a month you’ll get a £25 voucher

- If you deposit £25 to £29.99 a month you’ll get a £30 voucher

- If you deposit £30 to £34.99 a month you’ll get a £35 voucher

- If you deposit £35 to £39.99 a month you’ll get a £40 voucher

- If you deposit more than £40 a month you’ll get a £45 voucher

And until 13th April 2021 there’s an extra £10 added to all gift cards.

You get the reward voucher within 28 days of your first payment, and you can use the voucher at shops including John Lewis.

Buy vouchers via your Friendly Rewards account

Once you’ve done this, you’ll be sent details to access your Friendly Rewards account, and you can start taking advantage of the discounted gift cards.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

How to get up to £150 extra cashback on your ISA

If you want to walk away with a potentially larger profit thanks to cashback, then you need to follow these steps. It’s all pretty easy, but I do have a few major warnings, which I’ll get to in a bit.

Go to a cashback site

Go to a cashback site – ideally TopCashback or Quidco. Then search for Scottish Friendly. You might see a few options. To get the most money you probably want the Investment ISA option rather than the Junior ISA.

Andy’s Top Tip

If you’ve never used Quidco or Topcashback then check out my page with the latest welcome bonuses for new users. They can be worth up to £17 on top of other cashback you earn.

You won’t get the bonus for getting the ISA with Scottish Friendly so you’ll need to also shop elsewhere, but there are thousands of brands to choose from, including M&S, ASOS and Booking.com.

Choose an ISA

*Rates correct at the time of writing *

Choose one of the Scottish Friendly cashback offers. At the time of writing, you can get £200 from Quidco and £150 from TopCashback.

*THE REALLY IMPORTANT BIT 1 – Investment ISAs*

As I said earlier when you open an investment ISA, your money is at risk. Hopefully the money you put in will go up in value, but it could fall.

And there will be fees which will reduce this initial investment. Even if you’re planning on opening an investment ISA, Scottish Friendly won’t necessarily have the lowest fees, so it’s worth comparing your options. I’m only suggesting Scottish Friendly for an ISA because of the work perks trick, not as an ISA.

And do read all the terms and conditions of your ISA so you know what you’re committing to.

*THE REALLY IMPORTANT BIT 2 – Getting your cashback*

To qualify for the cashback there are two key requirements. One is to invest the money for at least 60 days.

Plus, the cashback will only be paid once you’ve made payments into your ISA at least equal to the value of the cashback. So if that’s the £200 cashback, you need to invest at least £200.

But there’s another clause which will probably reduce the cashback you get. The only Scottish Friendly ISA available via the cashback sites is a My Moneybuilder Select ISA – not the ones mentioned above.

These have a £50 exit fee if you cancel and cash out the ISA earlier than five years. So you either need to be prepared to leave your investment in the ISA for that time, or lose some of your cashback.

And don’t forget cashback can take a while to pay out – so you might not get the extra money for months.

Don’t forget you can still go direct and get the bonus gift card without having to lock in your money.

As ever with cashback sites, make sure you follow the instructions to ensure your click tracks.

Example

So if you can invest £100 a month for two months, you’ll be eligible for £200 in cashback from Quidco.

If you then withdraw the £200 investment and pay the £50 early withdrawal fee, you will get around £150 back, give or take any loses or gains made on the initial investment and fees charged.

Don’t close the ISA down though as you want to keep access to the discounts and benefits described above.

After some time the cashback payment of £200 will be processed and available to claim from your Quidco account.

If you can afford it, you might want to keep the £200 in the ISA until at least five years have passed to avoid the early exit fee.

Do you know any other hacks that will get you access to work perk schemes without expensive membership fees? Let me know in the comments below.

Can you pay for the gift cards using AMEX?

I had a question on this one. I know you have to invest an amount equal to the cashback you recieve and keep it open for 12 months. There was another point on the T&C “Cashback will not be paid if your monthly payments are less than the stated offer amount”. Does this mean I need to invest the monthly amount for at least 12 or 16 months until the cashback is paid? or Can I sum up my monthly investments over 12 months and make that investment before 05th Apr 2022 and then start another isa in the next tax year?

Cheers

Barry

HI Barry, hmm not sure about that specific term and condition. You could contact the cashback site for clarification

Think this might be worth mentioning. The ISA you mention has an expensive charge of 1.5% per annum all in. However another ISA with Scottish Friendly only charges .5% per annum, which is a very significant saving. It’s called My Prime and needs a lump sum of £2000 or £100 a month regular payment. Now, you definitely won’t get a cashback when you take it out, but you will get the Vectis card with, as Andy has pointed out, huge savings. I’ve had this for some time and get the discount with Morrisons and Sainsbury’s. I also saved a lot at Go Outdoors last year. Marks and Spencer is another regular standby. Incidentally, I won a £50 M and S voucher from Scottish Friendly in a draw, though obviously this can’t be counted on regularly. I find that Scottish Friendly’s investment returns are good, but you’d need to do your own research on that one and let the buyer beware.

I’m a retired member of the Royal College of Nursing, this gives similar benefits. Costs £10 a year which I generally save on the first transaction.

I have paid in 3 lots of £1000, in 3 consecutive months, this to get the maxiumum £300 cashback.

TopCashback is now reporting that the cashback will be paid in 52 weeks! I wish to stop paying in any more.

The rules, as above, say

“Finally, the cashback will only be paid once you’ve made payments into your ISA at least equal to the value of the cashback.”

That’s a huge wait! Have they confirmed it or is it still pending?

It’s still pending, which is also worrying.

I’ve raised a ticket but TopCashback just sent a standard reply saying “With all cashback transactions we need to wait for the retailer to validate your purchase and confirm its eligibility for cashback. When they have done this the status will progress to Confirmed”

Given what I’ve paid in, surely it should be marked as “Confirmed”?

Hi Andy

Is this scheme by Scottish Friendly known as “My Benefits” by them.

I just wanted to make sure that what you are referring to is indeed what I mentioned.

Kindly clarify.

Thank you kindly.

Hi Simon, yes I think that’s it.

You say that you can reduce the balance and retain theVectis card, but I don’t believe this is the case. If a withdrawal is made which leaves less than £50 in the account, the account is closed. It’s still a good deal. Just stop the monthly payments, but leave the money already invested and save on discounted shopping.

It worked for me. But yes, if you’re happy to keep the money invested there’s no risk it will be stopped.

If you withdraw your investment before 5 years have passed you are charged £50 to do so, so not making any money on the lower investments per month…

Hi Jac, thanks for this. I’ve updated the article accordingly. It appears only one type of ISA is available when you go via a cashback site and it has this £50 early redemption charge. You can however go direct and get a smaller reward, between £15 and £45 – so that’s probably the best bet for most people.