Not all discounts, special offers and sale prices are as good as they seem

Worried you’re being misled by deals into thinking you’re getting a bargain? Here are few tools I use to make sure I’m getting a good price.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

Are you actually getting a good deal?

Something I hate as a bargain hunter is a fake deal. I see them all the time. I don’t mean fake as in the shop doesn’t exist, or the product advertised isn’t available. No, this is when a retailer tells you there’s a huge discount when that’s not quite the truth.

The headline says it’s 50% off. Or save £100. Maybe just a tenner. But look a little closer and the savings aren’t as they seem.

In reality, the price these misleading discounts are based on is original RRP (recommended retail price). And this is usually far higher than what the item has actually been selling for.

But it’s not as simple as saying these promotions are lies – there will be legitimate deals advertised in this way. Or the saving might still be decent, just perhaps not as big as the promo says.

Now an easy way to check if a discount seems reasonable is to compare the price at a few different shops. This is always worth doing, and you could save some cash. If you can afford it and feel it represents good value then that’s a win.

But it doesn’t necessarily mean you’re getting the best price. For that you need to take a look at price history.

Why price history matters

To know if the current price is a good price, you need to know how much it was sold for. Last week, last month, maybe even last year.

This gives you all the information you need to not just make a call about whether the discount shown is accurate, but also how it compares to the lowest recent selling price.

Is the RRP a fair reflection of the real selling price? Or is the sale price, even with the discount, pretty much the average selling price?

And you can use price history for items which aren’t on offer too. Is it on sale for a lower price than it has been for a while? Or is it worth holding back and hoping the price dips back down to the cost it was not too long ago?

Bad deals masquerading as good deals

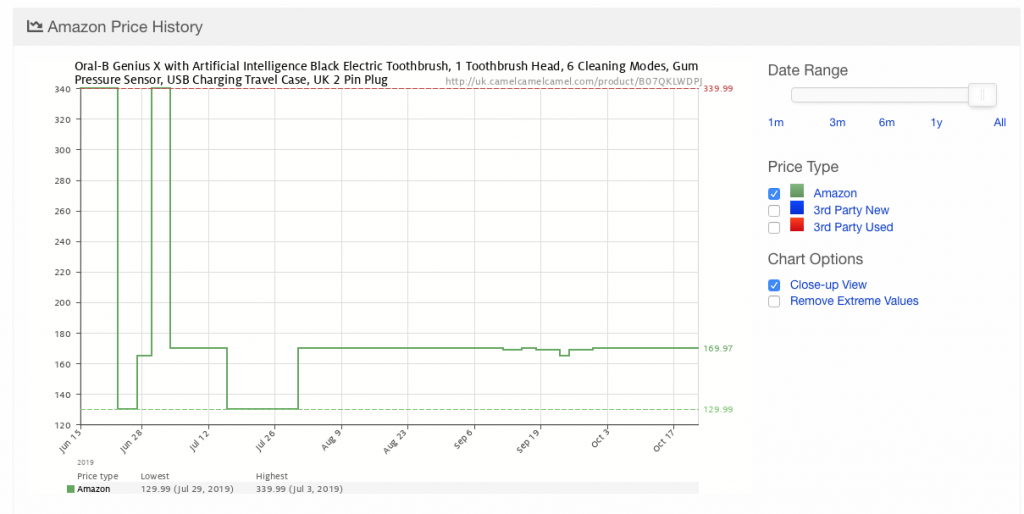

Here’s an example. A while back Boots was selling a top end Oral B toothbrush at half price. So you could pick it up for £150 rather than the staggering RRP of £300. A big discount on a big purchase.

But if you shopped around and looked at the real selling price, it became clear that this toothbrush is rarely sold at full price. In fact its usual selling price was actually around £150! So this isn’t a sale at all. It’s just how much it costs. In fact, it was possible earlier that year to buy it for £120 – at Boots!

So while if you did buy this toothbrush from Boots or elsewhere at £150 you aren’t necessarily overpaying, you certainly aren’t getting 50% off.

This trickery also applies to other promotion formats, such as a multibuy offer. It’s common to find that prices are higher during the promotion than they were a few days prior when they were in a different special offer.

Recently some posh pies in my local Waitrose cost £3.50 each, but you could get two for £6.50. So £3.25 a pie. But last month they were £3 each on a different offer!

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

Using price history tools

Thankfully checking these old prices is really easy for most retailers thanks to a series of websites that track the pricing data.

I love the price history feature. It lets me get geeky with my bargain hunting – but it’s also a quick and easy option for a casual check.

When you search for a product you’ll see a graph showing the ups and downs of the prices. With the best sites you can also expand a table to see just how much different retailers have been selling it for over time.

And they’ll usually let you see the price history for as far as a year, if not more.

The best price history trackers

There are three sites I tend to use when investigating the real price history.

Camel Camel Camel for Amazon price history

This tool is only for Amazon, but whether you’re buying something on Amazon or not, Camel Camel Camel is a really useful indicator of a broader price history as other retailers tend to follow Amazon.

This means in most cases, even if the current price at Amazon isn’t the best price, there’s a good chance you’ll get a sense of how much you should be paying.

A quick short cut for Camel Camel Camel is to use the product code rather than typing in the product name. Doing this ensures you’re getting the exact product you’re after. You can find the code in the URL or in the product description.

Featured switching deal

Featured switching deal

Our top pick

Our top pick

- Switch bonus£200

- Offer endsUnknown

- Extra bonus£25 Amazon Gift Card

- FSCS Protected? Yes

- Switch bonus requirements Switch using the Current Account Switch Service and close your old account within 60 days of starting the switch

- Deposit requirements Deposit £1,500 in the first 60 days from opening the account

- Direct debits transferred over Set up two Direct Debits before or after the switch from a selected list of household bills

- Existing customers? Can't have held any Santander current account on 1 January 2025

- Restrictions Can't have received a switching bonus from Santander already, offer limited to once per person

- Eligible accounts Open a new or hold an existing Everyday, Edge, Edge Up or Edge Explorer current account

- £25 Amazon Gift Card requirements To qualify for the gift card, you need to complete a full switch using CASS, and make five debit card transactions within 30 days of opening the account.

PriceSpy for price history at other shops

For most other shops I use PriceSpy. Though it’s not my favourite comparison site, it does have the best price history function.

PriceSpy has a really good option where you can see the individual price changes at different shops. Click on the price history graph in the top corner of a product page and it’ll open up to show a bigger graph and a table with all the different retailers selling the item. Then click the arrow to expand and you’ll see all the price changes.

Trolley for supermarket price history

You can even see how much an item has been selling for at the supermarket using Trolley. It’s a bit limited as you’ll only see the lowest price across all retailers rather than one by one, which can be skewed if one retailer always sells an item for less.

Still, it’s handy as a quick way to check if that bottle of wine that feels like it’s always on sale, really is. You’ll need to click the graph option to see the ups and downs.

What to watch out for

As much as I love these tools, they aren’t perfect. With PriceSpy the graphs present the lowest selling price over the time displayed. That’s handy but you don’t know for sure where this was – or if it’s a legitimate seller.

You can also only generally see the prices at places that currently sell the item. This makes it harder to get an idea of a real price for older and clearance items.

It can be tough too to compare prices and price history when retailers have exclusive models. I’m also wary slightly with PriceSpy that it might not show when items are out of stock. I’ve spotted occasions where a very low Black Friday price has been shown for a long period of time but the item was not actually available. This is pretty rare though.

And of course, these prices listed are the selling prices and often don’t take into account extras like discount codes or special member sales such as Prime Day – so it could be that the lowest price shown isn’t actually the lowest ever price.

Even with these slight negatives, I think using these tools is key to making sure you’re getting the best price possible – and not get caught out by fake deals.