I found two TVs on sale which were practically the same – but had a £250 difference in price.

Sometimes a new version is blatantly different, even if the main reason for change is to generate more sales. A new football kit, for example, will look different to the previous season’s. Sometimes the updates are hidden but make a difference, such as the change from an iPhone 7 to an iPhone 7S.

Now, whether they are worth paying for is up to you. The older versions still do the job they were designed for, but at least there are tangible changes to partially justify shelling out for an upgrade. But that’s not always the case.

A tale of two TVs

One of the families I recently visited as part of Channel 5’s Shop Smart Save Money was after a new TV. Prior to my visit they’d spotted a 49″ Sony model at Curry’s. The cost, a hefty £799. My job was to help them make some savings, and mum Debs had already searched online and found it for £50 less at Huges Electrical. I couldn’t beat that price by much, just a few per cent using cashback sites. But I noticed this was a brand new model. So I had a look at the long and confusing model number: Sony KD49XF7073SU.

The model number is the key to work out exactly what you’re getting. It just doesn’t make much sense! However a quick Google and I found an explanation of the different characters. For this TV, ‘KD’ just means it’s a Sony Bravia TV while ’49’ is the screen size. ‘X’ signifies it’s a 4K TV. The next one is the model year, with an ‘F’ telling us it’s a 2018 release.

The next two digits show the spec, so the higher the number, the more features it has, while the next two numbers are cosmetic such as different colours. While the final two letters (if they are mentioned) tell us it’s got a UK plug.

So armed with this information I had a quick search for Sony TVs with similar model numbers And not only did I find a similar number, I found an exact match with just one difference. There was an ‘E’ for 2017 in the model number. And this Sony KD49XF7073SU cost just £499.

Ok, you’re probably thinking a newer version of something should be better right? Why would you upgrade something that’s perfectly fine if you haven’t improved it somehow? And normally that’s the case. But when I compared the specifications for these two TVs on the Sony website, all the features looked the same.

In fact they were so similar the only differences I could find were the inbuilt speaker and the stand design. Ok, you might prefer the look of the 2018 stand. And the speaker might be better. But are they worth £250? If like the family after the TV it was going to be hung on a wall, the stand became irrelevant, and many people plug in a soundbar so it doesn’t matter what the built-in speakers are like.

So in this instance, the latest model isn’t an upgrade, it’s just a way for Sony and the retailers to make more money. But you can use it do save decent money as retailers look to clear out older versions by cutting prices.

Still want the new model?

Comparing prices is obviously a great way to save money, but while you’re at it, also check out the price history. This could help you work out whether just waiting a few weeks or months could save you a little more cash.

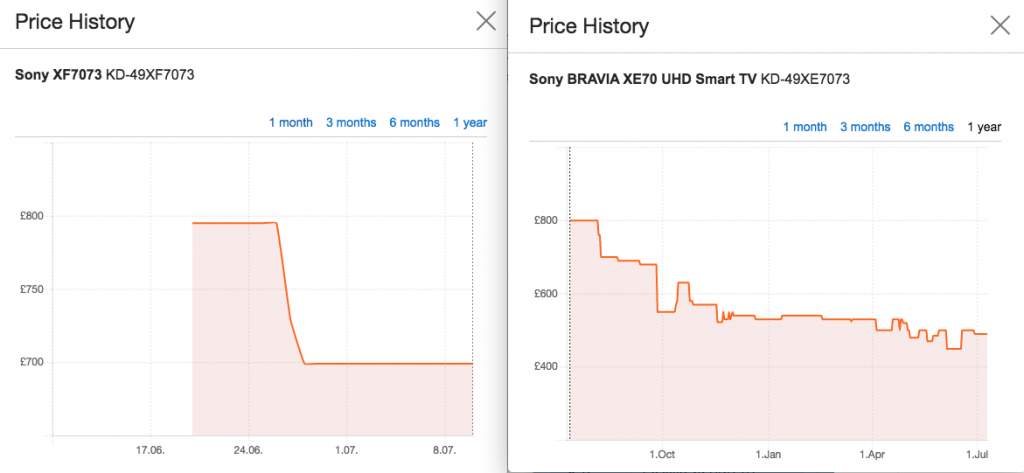

The 2018 model of this TV was released in mid-June at £799, which was the price listed when I did the research. Using price comparison site Idealo I can see that within two weeks it was available for as low as £699. So with most tech, this suggests it’s not worth getting it in the first few weeks.

And if it follows the same pattern as the 2017 model, it could well drop again in a few months. The 2017 model was below £600 by late September. So finding out the price history of similar models could help you know the best time to buy.

How to decipher model numbers

In most model numbers each character represents some variation from a similar version. It could be the age of the model as with the TVs above, or it could be additional features – which you won’t necessarily need.

For example, when I was looking for a new oven I found one letter difference between the two models. One ended with a ‘B’, the other with ‘BP’. The price difference was £240. so what was the ‘P’? It essentially stood for “Pyrolytic” – an enhanced self-cleaning mode. Yeah, nice to have, but not for £240.

Once you’ve worked out the differences, use this information then to swap characters, or ditch them completely to see if there’s a similar but cheaper alternative.

Find a guide to model numbers

Ideally you’ll find a guide online like I did for Sony, though this won’t always be possible. But it’s worth searching, or even asking in store.

Look for obvious differences

If you look at a couple of similar models it doesn’t take long to work out some of the characters. An S might stand for Silver and a W for White. Easy. A higher number usually means it’s higher spec, and so on.

Other characters might require a little more work, but as with the oven I bought it can be worth it. Often all you need to do is read the description online and see if there’s a key word different, such as the Pyrolytic feature of the more expensive oven.

Compare features on the manufacturer website

Sometimes though, codes change significantly when a new model is released. When this happens it’s best to use the manufacturer’s website as you get to compare all the models, not just the ones sold by a retailer. You can then use filters to narrow down your search based on the features listed. Here’s an example.

Last week I spotted a Miele washing machine on special offer. Our current machine is working OK, but it’s over a decade old. Being Miele, the new one wasn’t cheap, but as it was from 2016 and not listed on the Miele website I assumed it was an end of the line model – meaning the clearance price could have been significantly less than the current model.

However, I couldn’t find it on sale anywhere else in the UK to compare, and there were lots of models with very similar codes. There’d be no point buying if the discount was only £50!

So instead I found the full specs for the washing machine on Miele’s Hong Kong website, then used the search function on Meile’s UK site to filter out any current machines without those features. I managed to nail it down to one model which was practically the same apart from one enhancement. The difference in price was £700!! However, it was still too much to splash out right now, as tempted as I was!

More on how I save money on appliances and tech

Cash Chats ep 58: How I get the best value on tech and appliances

Read more about the savings I found when I visited Debs and Neil

£1k challenge: Debs and Neil