Will interest rates go up again on 2 November 2023?

Currently, the Bank of England (BoE) base rate stands at 5.25%, the highest rate since April 2008.

It has increased significantly since December 2021 (when the rate was 0.1%) as the Bank attempts to tackle high inflation.

Despite inflation holding steady at 6.7% in August and September 2023, it remains much higher than the Government’s target of 2%.

The BoE is due to announce its next interest rate decision on Thursday 2 November 2023.

But will interest rates go up again in the battle to reduce inflation? Here’s what you need to know.

Some articles on the blog contain affiliate links, which provide a small commission to help fund the blog. However, they won’t affect the price you pay or the blog’s independence. Read more here.

Will interest rates go up?

Interest rates are notoriously tricky to forecast. That’s because they ultimately depend on what the BoE’s Monetary Policy Committee thinks is the best way of ensuring the UK’s economy is in a healthy condition.

Inflation remains relatively high at 6.7% – over three times the BoE’s 2% target. So there is continued speculation about whether interest rates may need to increase to combat high inflation.

Andy’s podcast

Listen to Cash Chats, Andy’s award-winning podcast. Episodes every Tuesday.

In theory, the stagnation of the inflation rate could indicate that the BoE’s strategy is working and they may choose to keep interest rates at the current level for the time being to measure the economic impact.

On the other hand, there could be a larger increase than has been anticipated to kickstart another fall in the inflation rate.

We’ll let you know what happens on the day here on the Be Clever With Your Cash website and our YouTube channel.

How high could interest rates go?

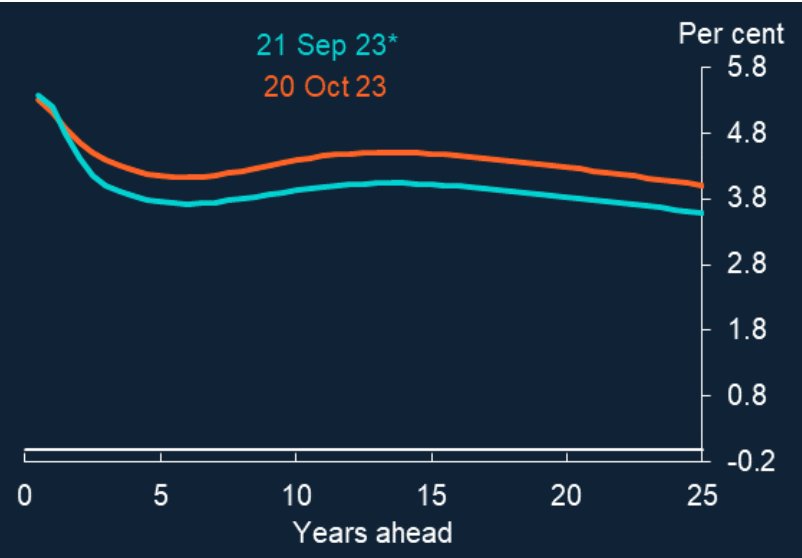

You can get a rough idea of how high interest rates are expected to go by looking at something called the overnight swap index (OIS) forward curve.

Now although it sounds a bit technical, this curve simply forecasts what interest rates could be in the future based on how investors are pricing interest rates into the market.

Currently, the OIS curve indicates that interest rates could reach around 5.5% by the end of 2023.

The orange line in the chart shows how much interest rates are likely to be based on market prices as of 23 October 2023.

However, there is speculation that interest rates could peak at 5.75% before starting to fall.

Now, although forecasts can be helpful to get an idea of what might happen, it’s important to remember that as with any economic predictions, they should be taken with a pinch of salt.

They are just a guide and rates may behave in a totally different way.

For example, back in June 2022 market predictions implied that interest rates would peak at 3.3% this year. In reality, the BoE surpassed that forecast by December 2022 when rates increased from 3% to 3.5%.

Could interest rates go down?

Interest rates may fall if inflation decreases in line with the BoE’s target.

At the last meeting in September, the BoE said that “CPI inflation is expected to fall significantly in the near term.”

Therefore, in theory, there is the possibility that interest rates may hold steady, or even begin to fall later in the year if inflation continues to decrease according to the BoE’s forecast.

However, as the market stands it’s unlikely that rates will fall anytime soon unless there’s a dramatic shift in the economy.

It’s also worth pointing out that even if they do start to fall – it won’t be by much. And, we probably won’t see interest rates go back to the historic lows we’ve had over the last decade and a bit.

The new norm could well be 3.5 – 4%, and it might take years to reach that. Especially if we do see more hikes in the rest of 2023.

Featured switching deal

Featured switching deal

Our top pick

Our top pick

- Switch bonus£200

- Offer endsUnknown

- Extra bonus£25 Amazon Gift Card

- FSCS Protected? Yes

- Switch bonus requirements Switch using the Current Account Switch Service and close your old account within 60 days of starting the switch

- Deposit requirements Deposit £1,500 in the first 60 days from opening the account

- Direct debits transferred over Set up two Direct Debits before or after the switch from a selected list of household bills

- Existing customers? Can't have held any Santander current account on 1 January 2025

- Restrictions Can't have received a switching bonus from Santander already, offer limited to once per person

- Eligible accounts Open a new or hold an existing Everyday, Edge, Edge Up or Edge Explorer current account

- £25 Amazon Gift Card requirements To qualify for the gift card, you need to complete a full switch using CASS, and make five debit card transactions within 30 days of opening the account.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

How does the base rate decision affect you?

The BoE base rate influences the cost of borrowing and saving which may directly impact your finances.

Typically, higher interest rates mean that the cost of borrowing becomes more expensive.

For example, if you have a variable-rate mortgage or a tracker mortgage, the cost of your repayments may increase if the base rate does.

Generally speaking, higher interest rates are good news for savers as providers tend to increase the return you can make from your money.

Currently, some of the best savings accounts offer around 5% AER with an easy-access account and 7% AER on a regular savings account or current account linked account.

Check out our article on what an interest rate rise means for you for more information.

Why is inflation so high?

Higher energy costs and increasing food prices are the main contributors to the high rates of inflation we see in the UK today.

The current inflation rate is 6.7%, over three times higher than the target rate of 2%.

Inflation is a way of measuring how much the cost of goods and services increases. This means that when inflation is high, things become more expensive.

And we’ve all seen the cost of living rise as prices have crept up across household bills and at supermarket checkouts.

If you’re concerned about managing price rises, it’s always worth checking whether you’re eligible for financial support.

The government’s benefits and financial support checker can help you find out if you’re eligible to claim help with the cost of living.