Here’s how you can avoid paying capital gains or dividend tax in the new tax year

When the new tax year begins on 6 April 2024, both the dividend and capital gains tax allowances will be cut in half, after already halving just last year.

This means that if you make more than £500 in profit from dividends and/or £3,000 from capital gains in the 2024/2025 tax year, you could find yourself having to pay tax. Here’s what you need to know, and how to avoid paying the tax.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

What’s the new dividend allowance?

As of the new tax year, which begins on 6 April 2024, the dividend allowance will be £500, down from £1,000 in the 2023-2024 tax year and down from £2,000 in the previous tax year.

What is the dividend allowance?

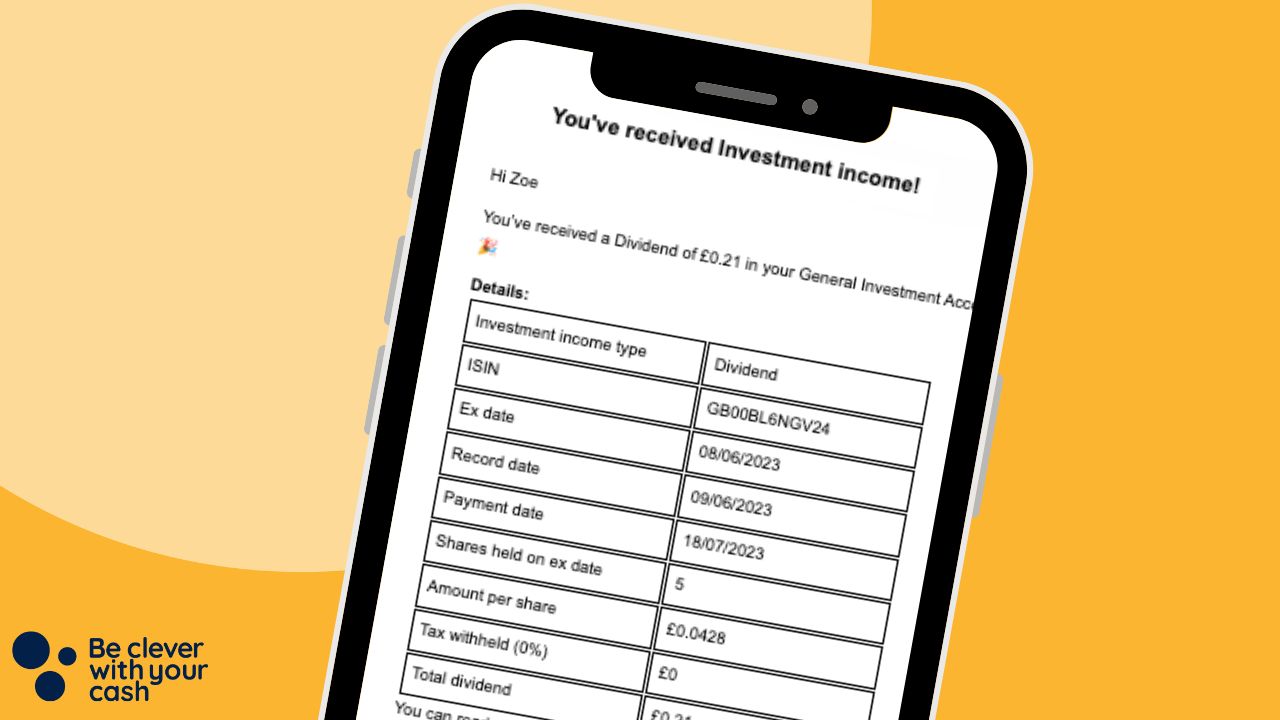

When you own investments, such as shares in a company, you sometimes get paid dividends. This is where the company chooses to share the profits with you. These are typically very small amounts per share — we’re talking pennies. But when you’ve got a lot invested, these can really add up, and for some, can pay them a regular income.

Everyone’s got a dividend allowance, which is the limit to the amount you can earn in dividends in each tax year before you have to start paying tax on it.

Once you’re above the allowance, the amount on top of it is taxed based on your income tax band.

Here’s the amount of tax you’ll have to pay for dividends above your allowance:

| Income tax band | Tax rate for dividends |

| Basic rate | 8.75% |

| Higher rate | 33.75% |

| Additional rate | 39.35% |

What this means: someone in the basic rate tax band who was making use of the full £2,000 dividend tax allowance in the 2022-2023 tax year would have had to pay £87.50 in tax in 2023-2024 and will have to pay £131.25 in tax in 2024-2025, assuming they earn the same amount in dividends.

What’s the new capital gains allowance?

The capital gains tax allowance will be £3,000 in the 2024-2025 tax year, down from £6,000 in the 2023-2024 tax year and from £12,300 prior to this.

What is the capital gains tax allowance?

When you dispose of investments, such as by selling them, any profits are known as “capital gains” . You can make gains up to the allowance in each financial year without having to pay tax, but once you’re above this, you have to pay capital gains tax on the difference.

Though this can apply to anything, from a second home through to fancy art, we’re focusing here on money you have in stocks and shares (importantly, outside of an ISA – we’ll come back to this).

There are rules that let you carry over an allowance if you made a loss in prior years, but this is one to talk to your financial adviser or tax adviser about.

Broadly speaking, the amount you’ll pay depends on your income tax band, how much your capital gains were and how much you earn.

If you’re a basic rate tax payer

Essentially, if you add your capital gains (less the allowance) to your income and you’re still within the basic rate tax band (£50,270) then you’ll need to pay 10% on your gains. If the total is above the basic rate tax band, the amount within it is taxed at 10% and the amount you go over by is taxed at 18%.

If you’re a higher or additional rate taxpayer

You just need to work out your capital gains over the allowance. You’ll pay 20% tax on this.

What this means: a higher rate taxpayer that was making full use of the capital gains allowance in the 2023-2024 tax year will see themselves paying £600 more in tax per year with the new changes.

This is a total of £1,860 more per year since the tax allowance was reduced from £12,300 in the 2022/2023 tax year, assuming capital gains are the same

What if I’m selling a second home?

If you’re selling a second home, then the rate is higher. This is 18% for basic rate taxpayers and 28% for higher and additional taxpayers.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

Can you avoid paying capital gains or dividend tax?

Yes. There are a couple of ways that you can avoid the additional tax. One way would be to make use of your ISA allowance and move your investments into a stocks and shares ISA.

You can move investments to make use of your partner’s allowance, giving you double the dividend, capital gains tax and ISA allowances between you. Of course, you can also do both of these combined.

If you’ve got a significant amount saved in savings accounts and investments outside of ISAs, you might wonder whether you should use your ISA allowance on your savings or your investments.

When it comes to savings, if you’re a basic rate or higher rate taxpayer, then you have the Personal Savings Allowance (PSA) of £1,000 or £500 respectively. This is the amount that you can earn in interest on your savings tax-free.

If you put your money in a decent easy-access account paying 5%, you’d have to have £20,000 saved to earn £1,000 in interest and £10,000 saved to earn £500 in interest in a year. So despite higher interest rates, most people are going to be protected by the PSA.

The allowances are higher for capital gains on investments, despite the reduction, but you need to be thinking about longer than a year. This is because you should hold investments for at least five years, to allow time for them to grow, and for the money made to grow too.

So that could mean, depending on how much you have, that you’re more likely to pay tax on investments than on savings.

Option 1: put investments in an ISA

If you’re not yet making use of your ISA allowance, you’re potentially missing out on tax-free investing. This allows you to invest or save up to £20,000 in each tax year where all of the profits you make are tax-free.

You can either start investing with new money, or move existing investments over – though as explained later, the latter isn’t as simple as it sounds.

Option 2: Use your partner’s allowances

While couples are treated individually when considering how much capital gains tax or dividend tax you owe, you’re allowed to transfer investments to your partner without paying tax for “disposing” of it, as you would if you transferred them to anyone else.

This means that you can divvy up your investments between you and make use of double the allowances. So if one of you in the relationship tends to deal with all of the money, which is common, you can take advantage of the unused allowances. You could do this with ISAs too, so you get a £40,000 allowance between you.

How to move your investments to an ISA

Sadly, it’s not as easy as shifting investments into an ISA, you have to do something called “Bed and ISA”. Essentially, it’s where you sell your investments that aren’t in an ISA and buy them again within the ISA.

Thankfully, a lot of providers offer a Bed and ISA service, where they’ll do all of this for you. If your investment provider doesn’t offer it, you’ll need to sell down your investments and buy them back within the ISA yourself. Be aware that this could take time, so try not to leave it to the last minute. And you’ll find that there’s a lot of demand for this service at the moment, thanks to the rules coming into play so soon.

It’s worth mentioning that this might be a decent time to reconsider your investment provider — check it’s offering all of the features you want now and take a look at the fees for the amount you invest.

Our podcast

Listen to Cash Chats, our award-winning podcast, presented by Steve Alderton and Editor James Andrews.

Episodes every Monday.

Important considerations for Bed and ISA

There are considerations that you should be aware of, and these might cost a fair amount of money up front, but this is with the intention of reducing your bill down the line. If you’re only marginally over the allowances, do some calculations of the fees to make sure it’s worthwhile.

Capital Gains Tax

As you need to sell your investments as part of the process, you may have to pay capital gains tax on your gains if they’re over the capital gains tax allowance (currently £6,000). This is likely to be less tax than if you did this after the changes come into effect, however.

Of course, you don’t have to move all your investments now if you will go over the allowance. You’ll still have a smaller allowance next year, and presumably in years after, so you can transfer over some now, and the rest later.

Fees to buy back investments

Most investment providers will charge you to purchase investments. The most expensive is Hargreaves Lansdown, which charges up to £11.95 per trade. There are apps that offer free trading, which can reduce this cost. You don’t typically pay a fee for selling an investment.

Do you have any of your ISA allowance left?

If you’ve already used your ISA allowance for the year, this won’t be an option for you. You could move as much as you’ve got left in order to reduce your tax bill somewhat.

You could potentially move your investments when the new tax year starts, but the new allowances will have come into play, so you might pay more in capital gains tax when you sell.

Pros of Bed and ISA

- Up to £20,000 per year saved with tax-free gains

- Move your investments before the allowances change

Cons of Bed and ISA

- May have to pay to buy back investments

- May have to pay capital gains tax when you initially sell

- £20,000 limit