The new 3-year bond from NS&I is out

Announced at the Budget in March 2024, this new government backed savings account will lock your money away for three years. Here’s how it works and how it compares to other savings accounts.

Some articles on the site contain affiliate links, which provide a small commission to help fund our work. However, they won’t affect the price you pay or our editorial independence. Read more here.

What is a British Savings Bond

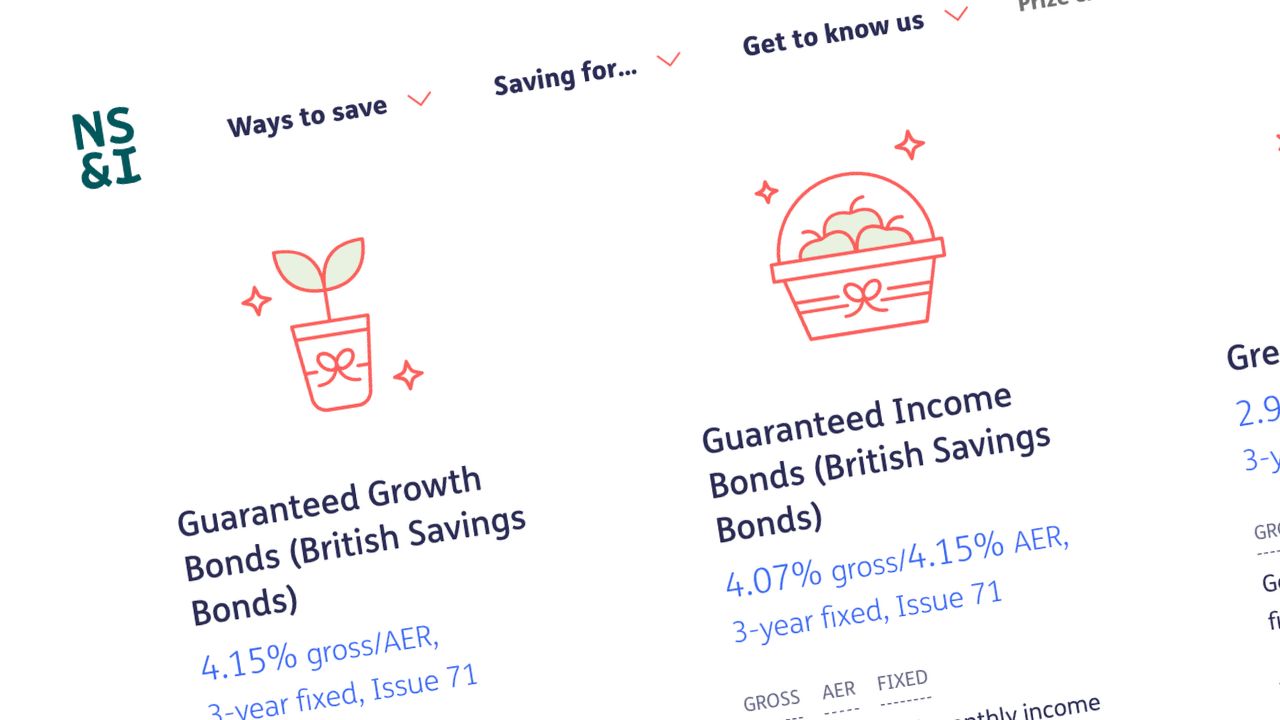

The British Savings Bond (let’s just call it the BSB), is a fixed savings account provided by National Savings & Investments (NS&I). There are two versions: Guaranteed Growth Bonds and Guaranteed Income Bonds.

Since it’s with NS&I rather than a normal bank or building society you get increased protection on your savings, with up to £1m protected. However, unlike NS&I’s Premium Bonds, the interest isn’t tax free.

If you open one of the BSBs you’re locking your money away for three years with no way to access it early.

How much does it pay?

The return, which applies for the full three years is 4.15%. Later we’ll look at how that compares to other options on the market right now.

When is interest paid?

The interest is either paid monthly (the Income Bond) or at the end of the term (the Growth Bond). That’s important as you’re liable for any tax on the interest when you’re able to access it, and there’ll be a larger lump sum after three years rather than in each year. Of course, tax is only taken if you go over your Personal Savings Allowance (or your personal tax allowance/starting savings rate if you’re a low earner).

How does it compare?

At launch you can get much higher than 4.15% from other providers, with the top account 4.67% from Zenith Bank, with a handful more just below this.

- Zenith Bank (4.67% AER fixed): min £1,000 / max £2m

- Oxbury Bank (4.66% AER fixed): min £1,000 / max £500,000

- Al Rayan Bank (4.65% expected profit rate fixed): min £5,000 / max £1m

- Close Brothers (4.65% AER fixed): min £10,000 / max £2m

- Hampshire Trust Bank (4.65% AER fixed): min £1 / max £250,000

- Secure Trust Bank (4.65% AER variable): min £1,000 / max £1m

If you were to save £10,000 in one paying 4.67%, you’d earn an extra £1,464. The BSB would pay £1,297 in interest. So that’s a difference of £167 over the three years. And the more you save the bigger the difference is.

Obviously rates will change, so check out our best buy savings tables for the top paying accounts.

How to open a British Savings Bond

BSBs are only available online, and you open them via the NS&I website. Once you’ve added your cash you can’t add more to the bond, but you can buy more as long as they’re still available. If you do this you’ll get whatever rate is then offered, and the three year clock will start afresh for the new money added.

Summary: are they worth it?

Andy’s analysis

There’s not a huge point to these bonds when the rate is significantly lower than those available elsewhere.

Though you get the increased £1m protection, up from the £85,000 provided elsewhere by the FSCS, do you actually need to have such large sums locked away for three years?

So I think for most people this is one to ignore.

Get the best of our money saving content every week, straight to your inbox

Plus, new Quidco customers get a high paying £18 welcome offer

NS&I British Savings Bonds

| Rate | 4.15% |

| Term | 3 years |

| Min | £500 |

| Max | £1m |

| Interest added | Either monthly or at term |